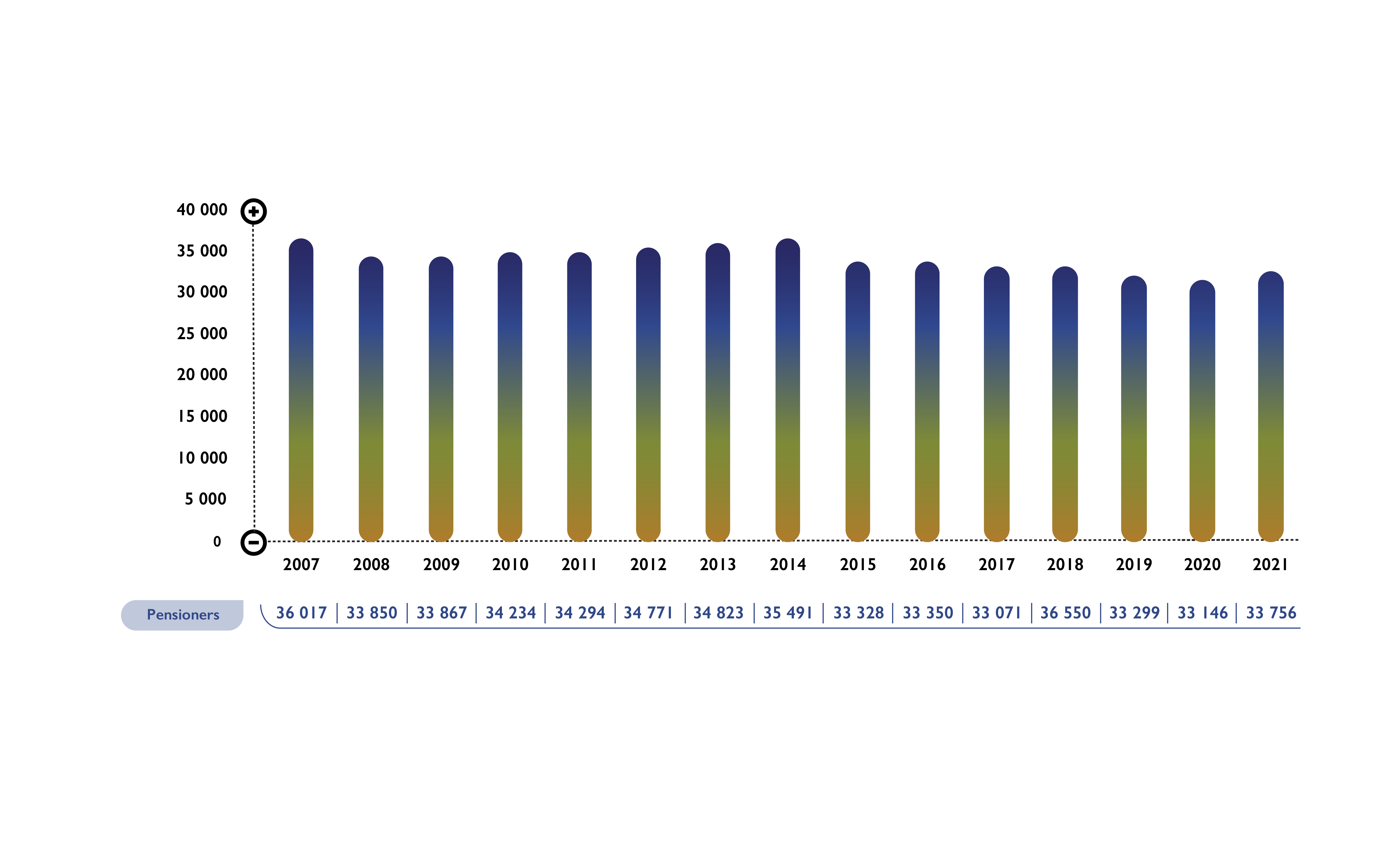

Pensioners of the EPPF are former in-service members who retire from the service of the employer OR deferred members (over the age of 55) who elect to start receiving a monthly pension from the EPPF.

Read morePensioners of the EPPF are former in-service members who retire from the service of the employer OR deferred members (over the age of 55) who elect to start receiving a monthly pension from the EPPF.

Pensioners of the EPPF are former in-service members who retire from the service of the employer and draw a pension from the EPPF.

Children over the age of 21 (major children) or any other beneficiaries/nominees of a death benefit can renounce their benefit by completing the Renunciation of Benefits Claim Form. Click here to download the form and submit to the Fund.

Spouses of deceased members and pensioners of the EPPF, as well as qualifying children in receipt of a pension are beneficiaries of the EPPF.

Normal Retirement

The EPPF’s compulsory retirement age is 65 years. However, in-service members may retire early from age 63 without penalties, subject to the employer’s conditions of service. The benefit is based on 2.17% of the in-service member’s annual average pensionable salary over the last year before retirement, for each year of pensionable service.

Early Retirement

An in-service member may retire early after reaching age 55 years. The benefit is a pension calculated in terms of a pension formula, reduced by the penalty factor of 3.9% per year for each year before age 63 years.

Ill-health retirement

An in-service member may retire at any age as a result of ill-health, provided that the Board of Trustees approves a recommendation by the EPPF Medical Panel in this regard. The benefit is calculated by making provision for a pension based on the in-service member’s pensionable salary and pensionable service accrued up to the actual retirement date plus 75% of the service that would have been completed by the in-service member from that date to the pensionable age.

Death after retirement

On the death of a pensioner, a lump sum equal to R3000 is paid to the surviving spouse or the estate;

Plus

The qualifying child/ren (biological or legally adopted children under the age of 21) are eligible for the monthly pension until the age of 21. A pension to the surviving spouse equal to 60% of the deceased pensioner’s pension at retirement before commutation, including any subsequent increases;

Plus

A further pension of 30% (for one eligible child) or 40% (for two or more eligible children) of the deceased pensioner’s pension at retirement before commutation, including any subsequent increases, in respect of any eligible children.

If there is no spouse’s pension payable, the percentage in respect of a single eligible child is increased to 60% of the deceased pensioner’s pension at retirement before commutation, including any subsequent increases. For two or more eligible children, the total percentage is increased to 100% of the deceased pensioner’s pension at the time of retirement before commutation, including any subsequent increases.

If there are no spouse’s or children’s benefits payable, a benefit equal to the excess amount of the lump sum, as specified below, over the total benefits paid to the pensioner until the time of death is paid to the estate. The lump sum comprises the following:

- A lump sum of R3000;

Plus

The greater of the two following calculations:

i. Twice the annual pensionable salary at retirement, less the pension benefits received since retirement;

Or

ii. The annual pensionable salary at retirement plus 10% of the final average pensionable salary per year of pensionable service, less pension benefits already received.

Triennially, the Eskom Pension and Provident Fund (“EPPF”), as per the EPPF Fund Rules, requires you, our pensioner, to complete an Evidence of Survival (“EOS”). The purpose is to verify your existence and to further ensure that our records/data are up to date for us to continue to pay your pension.

How do I submit my EOS?

Your EOS can be submitted through one of the following options:

1. USSD

The EPPF has launched its Unstructured Supplementary Service Data (USSD) functionality as part of the new channels. This service allows you to use your mobile phone to submit your EOS. Utilising the USSD platform means that you do not have to fill in any forms, go to the police station or worry about your form reaching the Fund on time:

NOTE: Please follow the guide on the link below, should you require assistance:

2. Electronic Form (e-Form)

For those that have access to the member portal an e-form is available for direct update of your record. Follow the guidelines outlined in the guide on this link: EOS e-Form Guide. Please ensure that you are registered on our safe and secure member portal.

Pensioners who have not yet registered, please register here and follow the guidelines outlined in the getting started manual. Click here to access the manual.

To upload scanned copies of your EOS form on the member portal, please follow the guidelines by clicking here. Documents must be less than 5MB and in PDF.

3. Physical Evidence of Survival (EOS) Form

The option of physical Evidence of Survival (EOS) is still available.

To return the forms to the Fund, e-mail a copy of the form to webupdate@eppf.co.za

What happens if I don't submit my EOS form?

If the Fund does not receive your EOS by the payroll closing date, the payment of your pension will be suspended until the EPPF receives your form. The implications of not submitting on time can be far reaching e.g. aside from not receiving a pension, certain third party deductions may not be processed, e.g. medical aid payments etc.

Are widows; widowers and guardians with minor children required to submit an EOS?

Yes. Widows, widowers, and guardians with minor children in receipt of a pension, as well as disabled children in receipt of a lifelong pension, is required to submit an EOS. The following should be noted:

Pre-Retirement Counselling

All members exiting the Fund are required to meet with a Retirement Fund Consultant (RFC) six months before their exit. The purpose of the counselling is to assist and provide you with information needed to make an informed decision when retiring. The RFC will also guide you as to what is required in the completion of the Retirement application form.

Retirement application

The member with the help of Human Resources (HR) must complete the application form.

This application form is used to process the pension as per the member’s instruction.

If previously divorced, members are encouraged to submit their divorce documents to the Fund to prevent delays in processing as the divorce documents are to be reviewed by the Fund’s legal team.

Documents

All documents requested on the application form must be provided to the Fund before the member’s exit where the quality assurance pertaining to the documents can be completed. These can be provided electronically.

Last Contribution

The EPPF will wait for the final confirmation and the last contribution. The contributions are received from the employer by the 7th of the month after your retirement and once allocated. Thereafter, the applicable interest rates are loaded at which time the claim processing commences.

Calculation

The member’s final retirement calculation is done in accordance with the Fund rules.

Tax

The retirement calculation is sent to SARS to confirm the tax deductible on the benefit.

Cash lump sum

The member is paid the Nett cash lumpsum value if he/she has opted for that.

Monthly Pension

The arrear monthly pension is loaded along with any deductions as indicated by the member. Thereafter, the pension will run monthly by means of the EPPF’s payroll system.

Letter

The member is sent a welcome letter providing them with their monthly pension value and the tax certificate.

Pensioner Card

The card is produced and posted to members which enables them to get discounts, this could be store or region specific.

The Fund is notified of the death by a family member or via the monthly payroll which does an upload from the Department of Home Affairs.

The applicant needs to complete a Death Application form. This form provides information that the Fund requires to load the spouse and/or eligible children.

The applicant is to provide the Fund with the relevant supporting documents as indicated on the application.

The final pension value is calculated in accordance with the rules of the Fund.

The monthly pension values along with any deductions as indicated on the application is loaded.

The arrear monthly pension is paid. Thereafter the pension is run by means of the EPPF’s payroll system on a monthly basis.

A payment letter is sent to the beneficiary(ries) providing them with the details of their monthly pension.

A payslip is provided to each recipient of a pension on a monthly basis.

Please complete a Consent to Receive Email Payslips and Correspondence form which is available via the member portal. Once you have completed the form, please fax or post it back to the EPPF. Click here to log on to the member portal and access the form.

The spouse’s pension is payable for the duration of your lifetime, regardless of whether you remarry or not.

Depending on the investment performance of the EPPF, the Board of Trustees may declare a bonus which is payable in December of that year. Pensioners are advised in December of each year whether a bonus is payable through a newsflash.

There are various factors which contribute to your tax fluctuating:

In December there was a bonus paid so your tax deduction was different from other months;

In January there was a pension increase which also created a difference in tax payable;

In the February payroll medical aid contributions increased. Pensioners aged 65 years and older used to get a full medical aid rebate. However as medical aid contributions increase the taxable income decreases.

The new tax year begins in March. The Fund’s payroll system annualises tax based on the latest tax earnings and the last year’s tax tables. Since the Fund’s pension payroll runs in advance on the 1st of each month, new tax tables for the new tax year are always implemented in the April payroll. However, please note that the new tax tables implemented in April are implemented retrospectively to the March payroll as per tax changes announced in the budget speech. This means that your tax on the April payroll will include the March payroll deduction adjustments. Your tax should then stabilise from the May payroll onwards.

Section 18(2) of the Income Tax Act has been repealed. This means that pensioners who are 65 years and older are no longer granted the full medical aid rebate by the employer during the tax year. Instead they are granted the medical tax credits by the employer according to the number of dependants they have on their medical aid. The section of the Income Tax Act that deals with medical aid tax credits is section 6A of the Income Tax Act.

Medical aid medical aid expenses (such as medication, doctor’s consultations etc.) and tax credits in respect of expenses are granted during the assessment year of tax returns. Should it happen that the pensioner has paid too much tax due to medical expenses not being deductible by the employer; SARS will refund the excess to the pensioner.

Medical aid contributions and medical expenses are granted in terms of section 6B of the Income Tax Act.

The Medical Scheme Fees Tax Credit for individuals is a credit which applies in respect of contributions paid by the pensioner who has a taxable income up to the last day of the tax year to a registered medical scheme. The amount of credit is based on the following values per month in the year of assessment in respect of which the contributions were paid in respect of the pensioner, the pensioner’s spouse and any other dependants.

The employer’s contribution is not disclosed on the payslip but it is disclosed on the tax certificate under the deduction code 4493. The pensioner’s own medical aid contributions are disclosed under code 4005. Both of these amounts are added to form the total medical aid contributions, which is listed under code 4497, the medical aid tax credits are disclosed on code 4116, the medical aid expenses will be disclosed on code 4120 as a zero value since EPPF is not privy to pensioner’s expenses so the medical expenses credit will be granted by SARS.

SARS gets this information when the Fund submits the tax certificates on the pensioners’ behalf during the employer annual submission time.

For taxable income rates, rebates and tax thresholds applicable to individuals for each financial year, visit the South African Revenue Services’ website on www.sars.gov.za.

The Evidence of Survival (EOS) form is used by the EPPF to ascertain whether people in receipt of a pension from the EPPF, who live outside South Africa are still alive and are rightfully in receipt of a pension. EOS forms are sent out annually to pensioners living outside South Africa and pensioners have a few months in which to complete them from the date on which the form is sent to them.

The EPPF always advises pensioners of the opening and closing dates for EOS form submission. Should the EPPF not receive your form by the EOS submission closing date, your pension will be suspended until the form is received. Please contact the EPPF if you have not received an EOS form or Click here to log into your profile and download the form.

Yes, you are still obliged to submit your returns as a confirmation of the information submitted by the employer on your behalf. In your instance, the EPPF represents the employer as the provider of a monthly income.

An AA88 is a garnishee order issued to the employer (the EPPF) against you by SARS for monies owed by yourself to SARS. Monies owed are usually due to non-submission of tax returns and non-payment of tax owed. An AA88 was previously referred to as an IT88.

When the employer or the EPPF receives this garnishee order it is required by law to comply and deduct the amount owed to SARS from your pension and pay it over to SARS on your behalf. This might affect your other deductions, as a SARS garnishee order takes precedence over other deductions.

Please contact your nearest SARS office to resolve your outstanding tax issues. You can contact SARS on 0800 00 72 77.

To change your banking details when you relocate to another country, you must submit the following documentation to us:

Original, certified copy of your identity document or passport

An original, completed, International Banking Form (IBF). The IBF must be completed by the bank to which you want to transfer your benefit, or by your foreign exchange service provider.

Click here to log into your profile and download the IBF.

Remember to also advise us of your change in address. Click here to contact us in order to update your address and other contact information.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique.